Today, we’re sharing with you the magic of Profit First.

But first, some truth-talk about money and being a REALTOR:

- Living on 100% commission is HARD.

- You’re not alone if you struggle with managing cash flow.

- The ups and downs in our business can be stressful.

- You aren’t the only one who uses a credit line to get you through the lean months.

- Almost every REALTOR I know has gotten into a tax mess by not having enough money saved up come tax time.

The good news? It doesn’t have to be like that. There’s a different way to manage your money.

Profit First, a book by Michael Michalowicz, is a life-changing way of managing cash flow for small businesses.

Profit First is a movement.

It’s a lifestyle.

It works for REALTORS.

It’ll work for you.

We implemented the Profit First book a few years ago and it changed EVERYTHING. Today, we want to share how Profit First works, specifically if you’re a REALTOR.

Profit First Core Principles

Traditional accounting has led you to believe:

- Sales – Expenses = Profit

- Profit is a magical line on your financial statement – and doesn’t reflect the actual cash you have.

Profit First accounting flips that traditional thinking on its head:

- Sales – Profit = Expenses

- Profit isn’t what’s leftover – it’s the goal. How much you can spend is determined by how much you have left over

- Profit isn’t imaginary – it’s actual CASH in the bank – the reward for your efforts

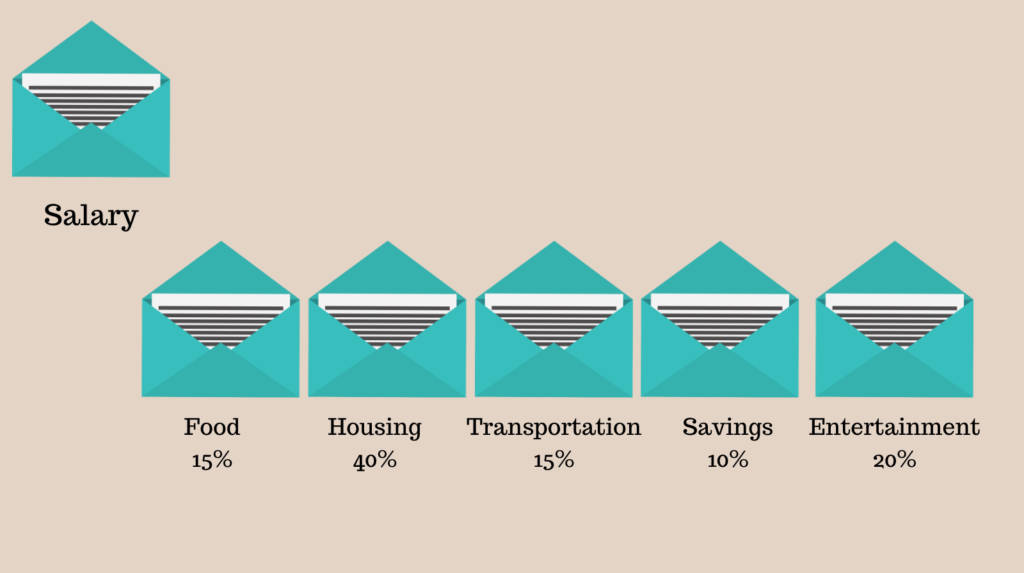

Profit First is based on the popular method of “envelope money management” which you may already be familiar with. The envelope system, in the personal money management/budget world, works like this:

- You receive a salary every 2 weeks

- You allocate a percentage of your salary to each of your spending buckets

- You can’t spend more money than what’s in the envelopes

The Envelope Method of Money Management

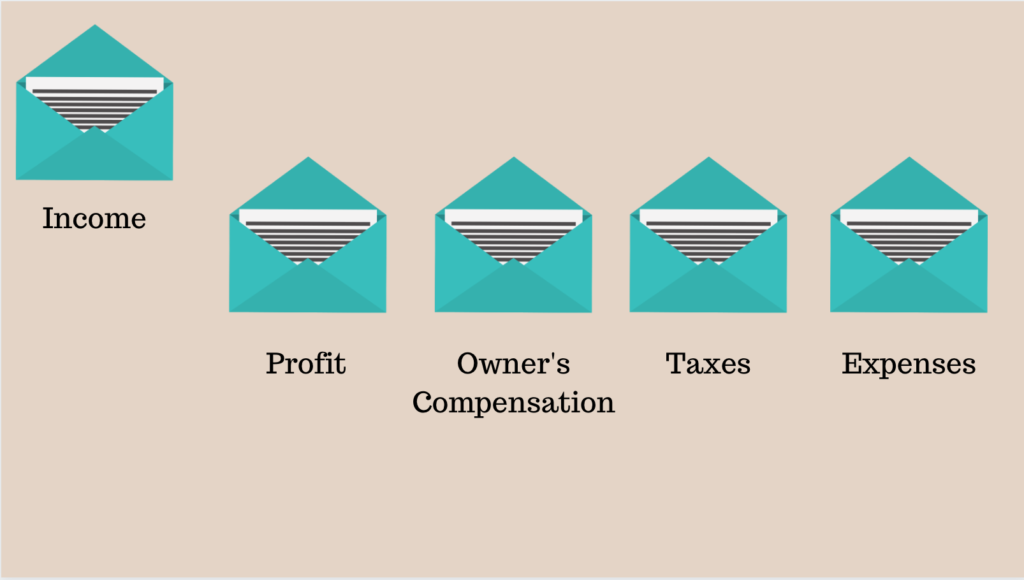

The Profit First Book applies envelope-thinking to small-business:

The Profit First Method

The Profit First book is based on 4 principles:

- Parkinson’s Law – If you have it, you’ll spend it. You know how you eat more at a buffet restaurant than you do if you order a la carte? Or how you use more toothpaste when you have a fresh tube than when you’re running out and you need to compromise? That’s Parkinson’s Law.

- The Primacy Effect – People place more significance on what they encounter first. When you focus first on profit (instead of expenses), profit becomes more important.

- Remove Temptation – Out of sight, out of mind. If you have chocolate in the house, you’ll eat it. Find a new home for your cash and you won’t spend it.

- Enforce a rhythm – Profit First is a habit – and you need to do it every month.

Important: It’s time to think of your business like a business. Your personal money and expenses should never mix with your business money and expenses. You should have dedicated bank accounts and credit cards for your personal expenses, and separate dedicated bank accounts and credit cards for your business expenses.

How Profit First Works (the quick-and-dirty version)

- Set up 5 bank accounts for your business – think of them as your ‘envelopes’:

- Income

- Profit

- Owner’s Compensation

- Taxes

- Expenses

- If you don’t already have a personal bank account and credit card dedicated to your non-business related spending, set that up too.

- Determine how you spent your money last year – how much of your income was allocated to Profit? To expenses? To taxes? How much did you pay yourself? This is the Profit First Instant Assessment and will help you determine your Current Allocation Percentages (CAPs).

- Determine how you WISH your income was allocated. What percentage of your income would you like to retain as Profit? What percentage should you spend on Expenses? What percentage should go to taxes? What percentage should you pay yourself? These are your Target Allocation Percentages (TAPs)

- Gradually, you’ll move from where you are (CAPS) to where you want to be (TAPS) by allocating your money into the different bank accounts. One of the great things about Profit First is that your life won’t be thrown into chaos all at once – you’ll make gradual changes that will add up over time and let you live the financial life you want to live.

- Every time you get paid commission, deposit your income into your INCOME bank account.

- On the 10th and 25th of every month, allocate that money into the PROFIT, TAXES, OWNER’s COMP and EXPENSE accounts – your virtual envelopes.

- Every quarter, you’ll get a bonus from the PROFIT account (half the balance) and start to build an emergency fund for your business (the other half of the balance). Spend your bonus on something fun. Don’t touch the rest.

Below, we’ll share our detailed guide to implementing Profit First for your real estate business:

Step 1: The Profit First Instant Assessment & Calculating Your CAPS

Don’t skip the Instant Assessment! You need to know where you are now, if you want to figure out a different way forward.

We’ve put together this handy Profit First for REALTORS spreadsheet to help. Just make a copy of it and follow the steps below:

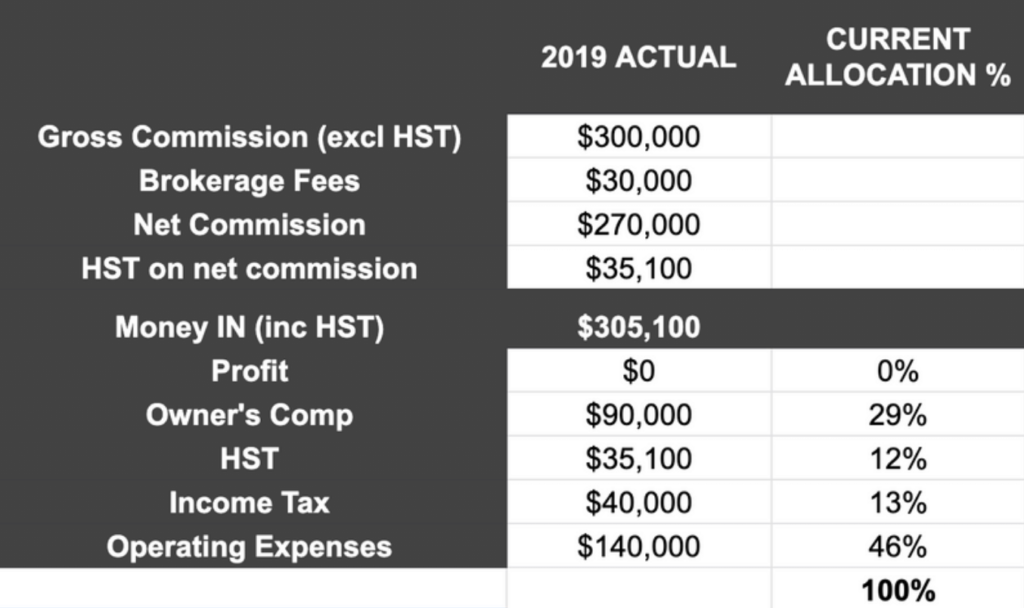

- How much income did you make last year? Put that number in the Gross Commission cell on the spreadsheet.

- How much did you give your brokerage? Enter the amount you paid in splits into the Brokerage Fees cell.

- The spreadsheet will automatically calculate your Net Commission – this is your real revenue, the amount of money you were paid.

- For Canadian REALTORS, we’ve added HST to the spreadsheet. Enter the amount of HST you collected in the HST on Net Commission cell. (For US realtors: use the US Profit First Spreadsheet and ignore this step.)

- Next up: Tally up all your business expenses for last year – all the money you spent to make your income. Enter that into the Operating Expenses cell.

- If you took any profit (ie cash that you didn’t spend and is in the bank) – enter that amount into the Profit cell. (Don’t feel bad if you didn’t take any cash profit, that’s how most REALTORS operate. And that’s about to change.)

- In the Tax line, enter the amount of money you’ve already paid to the government + any money you’ve saved and earmarked for taxes. For Canadians, split that money into the HST and Income Tax cells.

- The rest of the money? That falls into Owner’s Compensation – it’s the money you spent on yourself personally.

At this point, the spreadsheet will automatically calculate your current allocation percentages (CAPs). This is your starting point. It will only get better from here.

Your spreadsheet might look a little like this:

Step 2: Determine Your Profit First Target Allocations Percentages (TAPs)

Before we begin this part, I want to share an important mindset shift from the book:

Owner’s compensation is the money you get paid for working in your business; profit is the reward you get for owning it.

How exciting is that?

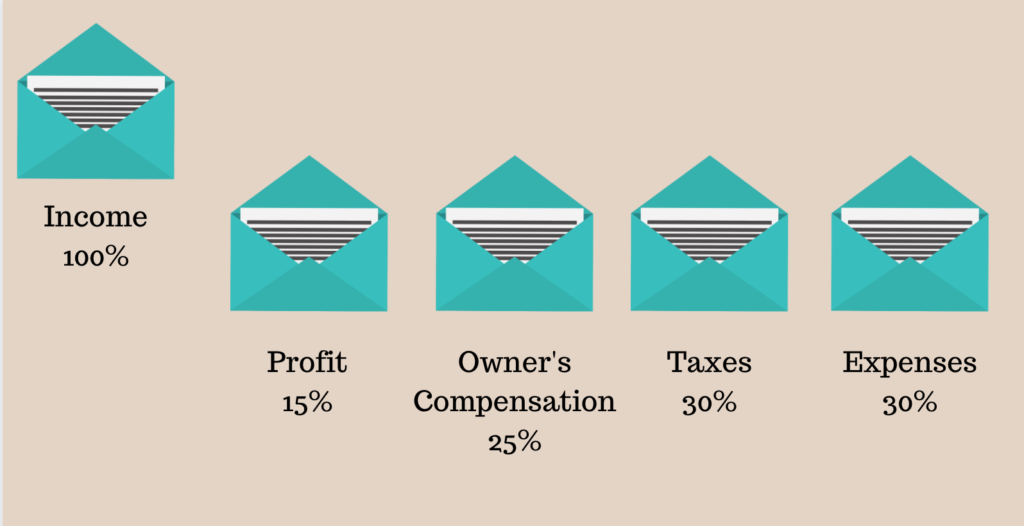

Here’s how you go about determining your Target Allocation Percentages (TAPs) – your ideal state of how you want your income to be divided. Back to the spreadsheet:

- Determine the target % of your income that will go towards PROFIT. 10-15% are typical targets for REALTORS.

- Determine the target % of your income that will go towards paying you, the OWNER’S COMP. This money will be used to pay you a regular salary – yes! – a consistent salary – that you can depend on to pay your personal bills. If you’re running a team or a brokerage, this number should be equal to how much you would have to pay someone to replace you if you ran off to a beach in Thailand. If you’re an independent agent, set this percentage to reflect an average of your worst 3 months of the year – that way you’ll always have money to pay yourself. (PRO TIP: Make this % work out 25% more than you actually will pay yourself, to adjust for revenue fluctuations.) Enter this percentage in the Target Allocation cell.

- Determine the % that you need to save for TAXES. Get guidance from your accountant and make sure to revisit this number with them every quarter, if your business is growing. Enter this number in the Target Allocation cell.

- Determine the % that’s left for EXPENSES. Remember, this is just paying the operating expenses of your business, not your personal expenses.

The spreadsheet will automatically calculate what the balances would look like if you were operating under your TAPs – it’ll show you:

- How much money you’d have in PROFIT

- How much you’d have saved up for TAXES

- How much you could pay yourself in OWNER’S COMPENSATION

- How much money you could spend on OPERATING EXPENSES.

If you think of your spreadsheet as envelopes, your TAPS might look like this:

Step 3: Determine Your Quarterly Allocation Targets

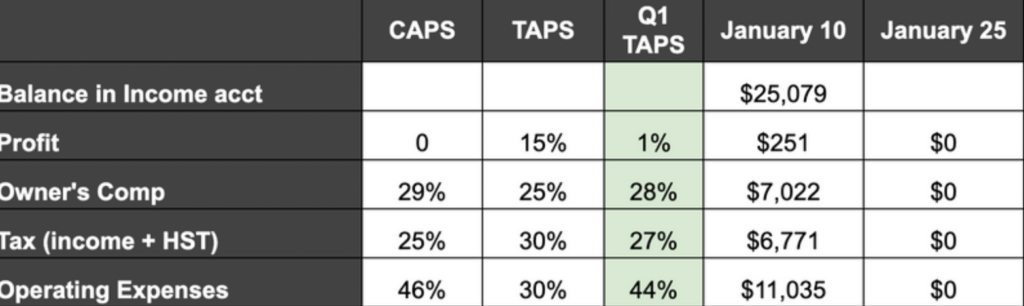

You’ll be setting quarterly target allocations to help you move from where you are to where you want to be. This is a slow process – aim to be better by 3% TOTAL each quarter. For example:

- If your CAPS were:

- Profit: 0%

- Owner’s Comp: 29%

- Taxes: 25%

- Expenses: 46%

- Your first quarter targets might be:

- Profit 1%

- Owner’s Comp 28%

- Taxes: 27%

- Expenses: 44%

The Profit First Allocations: the 10th and 25th of Every Month

Remember: all your commission income gets deposited directly into your INCOME account and stays there until it’s time for your monthly allocations on the 10th and 25th of each month.

You’ll want to use the second tab of our Profit First for REALTORS Spreadsheet to help with the calculations. On the 10th and 25th of each month, you’ll need to:

-

- Transfer money from your INCOME account into your PROFIT, OWNER’S COMP, TAXES AND EXPENSES bank accounts, according to your target percentages for the quarter.

- Transfer the salary you want to pay yourself from the OWNER’s COMP account, into your personal bank account (where you’ll pay your personal bills from). Don’t drain the account – the leftover will help fund your ‘salary’ in the months when you don’t take in a lot of income. Since this “salary” shouldn’t change, you could set it up as an automatic transfer if you like.

- Pay your business bills and expenses from the EXPENSES account.

- Don’t touch the money in your PROFIT account

- Don’t touch the money in your TAX account (that’s not really your money).

The allocation spreadsheet looks like this:

The Quarterly Distributions: the 1st of every quarter (Jan 1, April 1, July 1,October 1)

This is the fun part! Every quarter:

-

- Pay yourself ½ of the balance in your PROFIT account. Spend it on something fun.

- The rest of the balance forms your emergency fund – don’t touch it.

- Recalibrate your quarterly targets (TAPS) by 3%, adding and subtracting so that you move closer to your target. For example, you might:

- Increase the % allocated to PROFIT by 1 %

- Decrease the OWNER’s COMP by 1%

- Increase the TAXES by 2%

- Decrease the EXPENSES by 2%

- The key is that you’re making small incremental changes in the right direction, and building on them every quarter

How do I Start Profit First as a REALTOR?

- Open the 5 bank accounts for your business (and make sure you have an account for your personal spending/savings).

- Complete the Instant Assessment, showing how your money is currently allocated.

- Determine your target allocation percentages.

- Set your first-quarter targets allocations to help move you from where you are to where you want to be. For example: add 1% to Profit, add 2% to Taxes and reduce your Expenses by 3%.

- Transfer all the cash you have right now into the INCOME account – you’ll use this to seed the accounts until your first allocation.

- Using your new target allocations for the quarter, transfer money from your INCOME account to PROFIT, OWNER’s COMP, TAXES and EXPENSES.

From there, it’s really just a matter of:

- Depositing your income into your INCOME account moving forward.

- Making the appropriate allocation transfers on the 10th and 25th of the month.

- Taking 1/2 the profit every quarter and recalibrating the allocation percentages for the next quarter.

Questions? You’re not alone. Consider buying the book – ithas tons of information and tools (and there’s an audiobook too). AND: we have a Profit First for REALTORS Facebook group to help you with implementation.

Judith Varga says:

If I did not have a wife already, I would marry you ..lol

Tanya Nouwens says:

An absolute wealth of information here, Mel and Brendan. So incredibly generous of you to share it. I read (most of) the book and have been using Profit First since last summer. It absolutely makes a difference in how I feel about my business and how I operate it.

Liat Gat says:

Wow, great site with wonderful information! I’m helping my mom set up Profit First for her business as a Realtor and I was glad to find your specific advice and spreadsheets regarding commissions (since in my own business my Real Revenue is my Total Revenue). Great reference page. I will be sending her to this page as well so she knows EXACTLY what the plan is.

Rita Vermeersch says:

Just listened to the book and found it so easy to follow and a wealth of information. I wish I had read it 25 years ago when I began this real estate journey!

Kyle says:

Hey! Wow thank you for the in-depth overview for us hard working real estate agents! I just finished the book and now starting the system, one quick confusion though. What about investments? I would like to invest at least 15% of in income each year, does this percentage come out of operation compensation?

Brendan says:

I think that depends – do you want to save 15% of YOUR income? Then it would be 15% of your owners comp. It should not come out of your OPEX account, that would be just for paying the business expenses.

Or, you couLd use your quarterly profit distribution to go toward investments – but that would be kind of “extra” and harder to keep consistent.

One other option is you could add another account, just for investment savings. Start that at a manageable % and work your way up to a TAP like any others.

Personally, we are at the point where ALL the Profit distributions go to investments—we have gotten our Owners Comp to a level where it covers our lifestyle and we try to lock that in and not pay ourselves more. As the biz makes more money, that just stays in the biz as savings. (We are incorporated too, so that money stays invested in the corp, which is better for taxes. If we paid ourselves more $ just to invest personally, then we’d have to pay tax on that income from the corp…which defeats the point of the corp as a tax shelter)

Join the profit first for realtors Facebook group and you can ask others what they do!

Jason says:

Hey, first thank you X 1million! I am a new agent with no prior year income. Shall I just start with the common TAPS and then next year fill out my CAPS? Any suggestions are appreciated.

Brendan says:

There is a process to figure out what your initial starting targets should be, so to be honest I would probably either get the book or find detailed resources for it online… but my main advice would be to start conservative — around what you spend now, but with 1% to profit to get going, and then only ratchet things up very slowly.

Our business is unpredictable so resiste the temptation to redo all the numbers as soon as you have a few good months. Slow and steady, with minor adjustments no more than 3% total changes per quarter. Your goals will come into focus as you see where you spend, where you accumulate, and where you WANT to.

Good luck!